How Custom Fintech Software Development Sydney Helps Financial Firms Scale

Table of Contents

You already know your legacy platform is holding you back. Every quarter it gets harder to patch, slower to update, and more expensive to insure against a breach you can see coming.

That’s why custom fintech software development in Sydney has moved from a nice-to-have to a board-level priority. The financial services software firms have relied on for the last decade is now what’s standing between them and Open Banking, ASIC scrutiny, and the mobile-first experience their customers expect.

Here’s what’s changing, what the regulator expects, and what a serious rebuild costs in 2026.

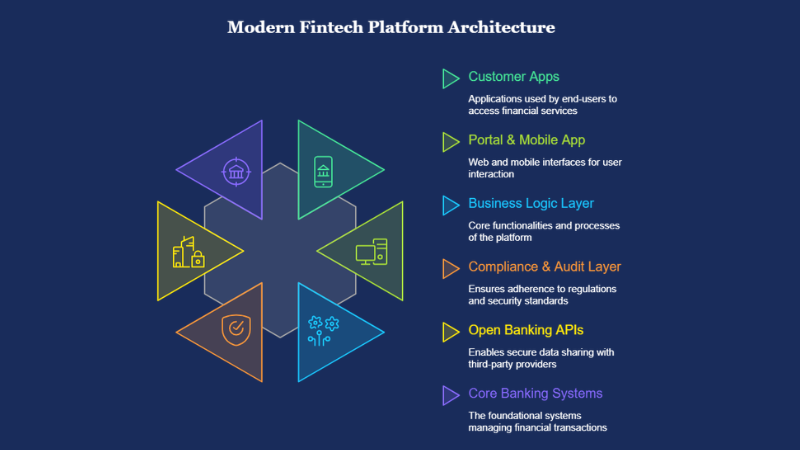

What Sydney fintech firms are building right now

Sydney’s financial services sector isn’t waiting for a five-year roadmap. Lenders want automated credit decisioning that cuts approval times from days to minutes, wealth managers want portals showing live portfolio data instead of overnight batch reports, and payment providers want settlement in seconds rather than days.

That’s driving three kinds of projects: lending platform development in Sydney, the wealth management software Australia advisers now put in front of clients, and fintech app development in Sydney teams can ship without blowing the budget.

None of this is hypothetical. It’s happening at firms your size, in your postcode, right now.

If your competitors are shipping faster decisions and sharper apps, the gap between you compounds every quarter you wait.

ASIC, AFSL, and CDR: the compliance requirements your software must meet

Custom doesn’t mean unregulated. If you hold an Australian Financial Services Licence (AFSL) or credit licence (ACL), your software inherits your licence obligations, including ASIC’s RG 271 rules on internal dispute resolution.

RG 271 sets a 30-day standard timeframe for resolving most complaints. Miss that window, and you’re not just annoying a customer. You’re creating a reportable breach.

The same logic applies to advice tools. Under RG 255, a robo-advice platform carries the same legal duties as a human adviser, and that liability can’t be shifted to a software vendor. If your algorithm gets it wrong, you wear the consequence.

That means ASIC-compliant software can’t be bolted on after launch. Audit trails, complaint handling, and escalation paths need to sit in the architecture from day one, not get added once a regulator starts asking questions.

Open Banking and API integration: what's possible in 2026

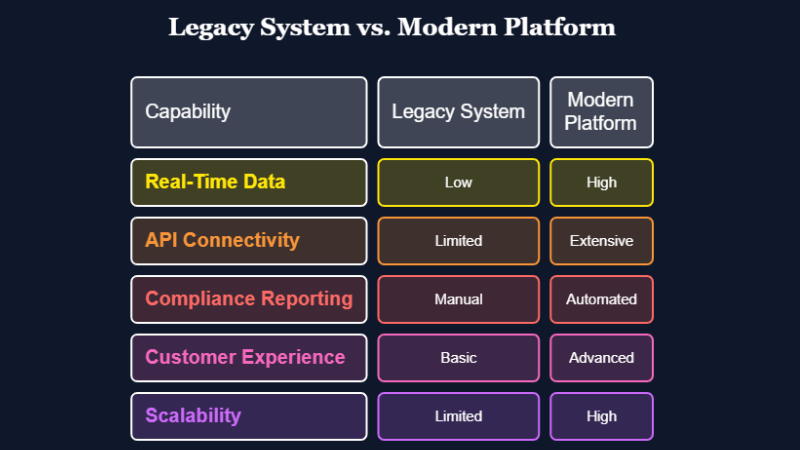

For years, lenders leaned on screen scraping, asking borrowers to hand over their online banking passwords so a third party could pull their transaction history. That workaround is losing ground fast.

Treasury’s CDR reset extends the Consumer Data Right to non-bank lenders from mid-2026, and brings buy now, pay later products into scope as well. The direction of travel is clear: structured, consented API data over scraped credentials.

That means real advantages for lenders who move early:

- Faster income and expense verification, without manual document checks

- Lower fraud exposure, since you’re no longer storing customer banking credentials

- Cleaner credit decisioning, because the data arrives structured instead of scraped off a webpage

If your lending stack still depends on scraping, you’re building on ground that’s shifting under you.

When legacy financial systems become a regulatory liability

Old systems don’t just slow you down. At some point, they become the reason you fail an audit.

A core platform that can’t produce a clean audit trail puts your AFSL at risk. One that can’t connect to CDR-accredited data recipients locks you out of products your competitors already offer.

Ask yourself three questions:

- Can your current system produce the dispute resolution records RG 271 requires, on demand?

- Can it connect to Open Banking APIs without a six-month integration project?

- Could it survive an ASIC information request without a week of manual data pulling?

A no to any of these means you’re not maintaining a legacy system anymore. You’re managing a liability.

Custom lending, payments, and wealth management platforms: what influences project cost

Complexity, not platform type, is what drives the cost of a fintech build. Credit decisioning, Open Banking integrations, audit logging, real-time reporting, regulatory compliance: each adds to the scope of work, and the price tag follows.

A straightforward client portal costs less than a lending, payments, or wealth management platform. The gap is wide: those platforms need to integrate with several third-party systems, handle sensitive financial data, and satisfy compliance requirements a simple portal never touches.

The upfront build cost is rarely the real risk. The real risk is choosing the wrong solution. A platform that can’t scale, opens up compliance gaps, or needs constant manual patching will end up costing more than getting the architecture right would have, from day one.

For regulated financial firms, that’s the real brief: software that grows with the business, holds up under security and compliance demands, and doesn’t turn into an ongoing maintenance burden.

We’ve mapped costs by project type in more detail in our guide to custom software development costs in Australia.

How Basecode approaches regulated financial software builds

We treat compliance as a design constraint, not a final checklist. Every regulated build starts the same way: we map your AFSL or ACL obligations against the architecture before we design a single screen.

Basecode runs custom software development, mobile app development, and systems integration for finance, healthcare, ecommerce, and resources clients across Australia. Our blended onshore and offshore delivery model keeps architecture and compliance decisions onshore, so your senior engineers sit in the same time zone as your compliance team.

We’ve covered the onshore vs offshore decision elsewhere in detail, including where each model saves money and where it adds risk. Security sits in the same conversation, and it’s worth reading our take on passwordless authentication before you lock in your architecture.

Starting a custom fintech software development project in Sydney? Get ASIC and AFCA into the first conversation, not the last.

If you’d like to talk through what a compliant rebuild looks like for your business, Basecode’s team is happy to walk you through it.

FAQs

1. Does financial services software in Australia need to be ASIC compliant?

If you hold an AFSL or ACL, yes. Your software has to support the obligations your licence already carries, including dispute resolution under RG 271.

2. How does Open Banking CDR affect custom software for lenders?

From mid-2026, CDR extends to non-bank lenders and buy now, pay later providers. Software still built on screen scraping will fall further behind the compliance curve each year that passes.

3. Can offshore developers build ASIC-compliant fintech software?

Yes, if the model is structured properly. Keep architecture, compliance logic, and data handling decisions with an onshore team, and the standard build work can run offshore without putting your AFSL at risk.

4. How long does it take to build a custom fintech platform in Sydney?

A straightforward client portal usually ships in three to four months. A full lending or payments platform with CDR integration and compliance built in typically takes six to nine months, longer if you’re connecting to multiple data holders.

5. How do I migrate from a legacy financial system without downtime?

Run the new platform in parallel, migrate data in stages, and cut over product line by product line rather than all at once. Done properly, customers shouldn’t notice the switch happening.